For the first time in 10 years, broad indices outperform Nifty 50 in market correction: MOFSL

As Dalal Street benchmarks moved towards all-time highs in late September, with the Nify50 still more than 1,600 points, or 6.2 percent, below the mark, broader indices including the Nify Midcap 100 and Nify Smallcap 100 indices registered a smaller fall than the underlying index during a market correction phase. Historically, when a correction—a slide of 10 percent or more from its recent peak—occurs in the Nifty50 index, the broader indices have registered corrections of up to 2-4 times, except in 2024, according to the dealer. Motilal Oswal Financial Services Ltd (MOFSL).

According to the brokerage, as of the end of November, while the Nifty stood at 8.0 percent below its all-time close, the midcap and smallcap indices were 7 percent and 5 percent below their highs. In other words, it is the first time in 10 years that the midcap and smallcap gauges have fallen below their large counterparts during the Nifty index correction. Technically, a correction is defined as a fall of at least 10 percent from the most recent high.

What has helped the midcap and smallcap indices in the performance category apart from the performance in the Nifty50?

Incessant net selling by foreign institutional investors (FIIs) led to a sharp decline in large caps, while strong retail and domestic investor (DII) flows led midcaps and smallcaps to outperform by a wide margin during the recent market correction, according to the Financial Services of Motilal Oswal.

Here is a comparison of movements in Nifty 100, Nifty Midcap 100 and Nifty Smallcap 100 compared to technical corrections in Nify50 over the last 10 years, as highlighted by MOFSL:

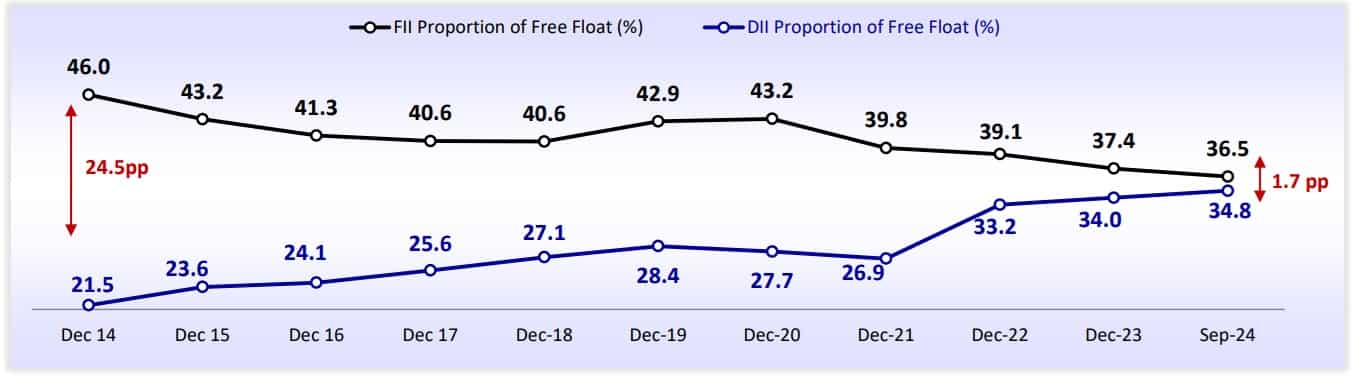

DII vs FII divergence hits multi-year low

Over the past 10 years, there has been a significant split in foreign institutional investors and the balance of domestic institutional investors.

“Incessant FII selling and DII buying has led to a significant shift in ownership in the Indian equity market… FII/DII ownership, as a proportion of free float, is down 950b/up 1,330bp from Dec’ 14 to 36.5% / 34.8%,” according to the brokerage.

Look at the gradual convergence of FII vs DII ownership

Largecap’s contribution to market capitalization is very low

A sharp rise in midcap and smallcap valuations over the past 10 years has led to a sharp decline in capital market contributions for the large segment, according to brokerages.

The market contribution of large caps decreased by 1,500 points from March 2020 to 60.4 percent in November 2024, while those of mid-cap and small-cap stocks increased to 19.1 percent and 20.5 percent, respectively, according to the report. Motilal Oswal Financial Services.

The rupee has been more stable than many of its emerging peers over the past decade

Over the past decade, the rupee has remained more stable than its emerging market peers. It remains “one of the most stable currencies in emerging markets”, according to MOFSL.

Additionally, the rupee has continued to be less volatile than other major currencies in 2024 so far.

A good measure

According to the brokerage, the Nify50 index’s 12-month trailing price-to-earnings ratio, 23.2 times, stands at a premium of about 3.0 percent to the long-term average (LPA). At 3.7 times, the trailing 12-month price-to-book ratio is 18 percent above its historical average of 3.1 times, according to MOFSL.

On the other hand, the 12-month forward price index average stands at 20.5 times, close to its long-term average, and its 12-month price-to-book average is 3.3 percent, marking a percent premium. -16 to its historical average of 2.8 times.

Meanwhile, India’s mcap-to-GDP ratio rose to 138 percent from an all-time high of 146 percent recorded in September 2024, though it is above its long-term average of about 85 percent, according to the business.

“For midcaps and smallcaps, market cap-to-GDP ratios continue to trade at historic highs, with all microcaps now outperforming midcaps,” added MOFSL.